Property Solvers’ analysis of HM Land Registry data has recently revealed that the number of cash house sales in England and Wales has fallen by 45% over the past five years.

Between 2020-21 and 2024-25*, annual cash transactions dropped from 799,592 to 437,903 – a reduction of more than 360,000 sales.

The decline has been consistent year after year, suggesting a sustained cooling of what was previously one of the market’s most resilient segments. Additionally, the data reveals that mortgaged transactions have fallen even more sharply, down 44% over the same period – from 2.01 million to 1.1 million.

Despite the downturn, cash sales still play an important role in keeping transactions moving. These deals often happen because they bypass the traditional mortgage process, reducing the risk of delays, surveys and lender withdrawals.

For sellers needing speed or certainty – and for buyers seeking negotiation power – cash transactions continue to offer clear advantages.

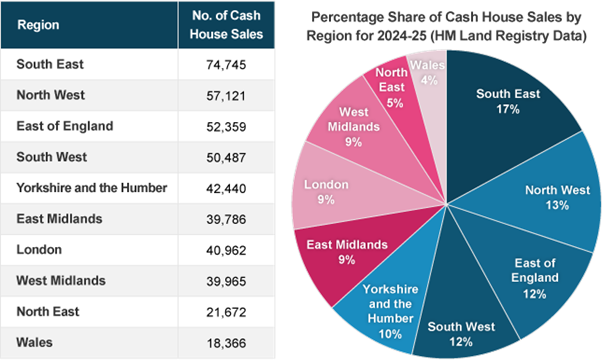

The South East Still Dominates Cash Sale Volumes

Regional data shows the South East remains dominant, accounting for 74,745 cash transactions in 2024–25, or around 17% of the national total. The North West (13%), East of England (12%), and South West (12%) follow closely behind.

At the lower end of the scale, Wales and the North East continue to record the fewest cash sales, representing just 4% and 5% respectively.

According to Ruban Selvanayagam, co-director at Property Solvers: “The South East remains ahead because homeowners there have built up more equity and are less reliant on borrowing. Many are downsizing or helping family members buy outright, which can keep cash transactions strong even as the wider market cools.”

What’s Driving the Fall in Cash Sales?

Selvanayagam argues that the fall in cash sales reflects shifting incentives for investors and equity-rich buyers.

Higher interest rates have made cash, gilts, and even stock market funds more rewarding. With 4-5% returns available elsewhere, property – with its costs and risks – no longer looks like the easy store of value it once was.

Cash buyers have also become more selective, often waiting for price corrections or distressed opportunities. “From what we’re seeing through our auctions,” Selvanayagam says, “active buyers today are seasoned investors or cash-rich individuals using long-accumulated wealth. They’re still buying, but far more strategically.”

The buy-to-let sector has cooled as landlords sell or streamline portfolios, while older homeowners and inheritance-funded buyers are delaying moves amid cost pressures and slower probate processes.

There’s also less market liquidity. With fewer listings and cautious pricing, even cash buyers are struggling to find value. Overseas and high net worth demand has eased too, hit by a stronger pound and higher stamp duty surcharges.

A Pause Rather Than a Collapse

While the numbers may suggest weakness, Selvanayagam views this as a temporary recalibration rather than a long-term retreat.

“The fall in cash purchases mirrors a wider slowdown in the market,” he noted. “Buyers with or without mortgages are waiting for more clarity on where prices and rates will settle. It’s less about a loss of confidence and more about timing – people with capital are being patient.”

He believes activity could recover once borrowing costs start to ease and sellers adjust their expectations: “When we see rate cuts feeding through and prices stabilising, there’s every chance these cash buyers will re-emerge – and quite possibly drive the next wave of transactions.”

* Figures are based on the most recent HM Land Registry data available, covering the five-year period from July 2020 to July 2025. Each annual total reflects transactions completed between July and the following July (e.g. July 2020 to July 2021).