- New student numbers topped 600,000 for the second year in a row – with a further 618,000 starting in 2022/23 and 622,000 in 2023/24

- £7.8 billion of UK purpose built student accommodation (PBSA) was traded in 2022, +89% on 2021, despite the weaker economic backdrop

- 82% of investment has come from overseas in the past three years – with investors from the USA and Singapore accounting for 47% and 24% respectively

- Two-thirds of investors are looking to deploy more capital into PBSA in the next three years – with close to a fifth aiming to deploy over €500 million

- Canterbury, Durham and Glasgow have emerged as new hotspots for those looking to invest in new UK PBSA developments

- A broad range of lenders continue to show considerable appetite for PBSA opportunities, recognising the sector’s resilience and strong rental growth

The UK’s Purpose-Built Student Accommodation (PBSA) sector is continuing to go from strength to strength, according to global real estate adviser Savills. A shortage of supply combined with rising student numbers has resulted in strong rental performance, with over 7% growth forecast for 2023/24.

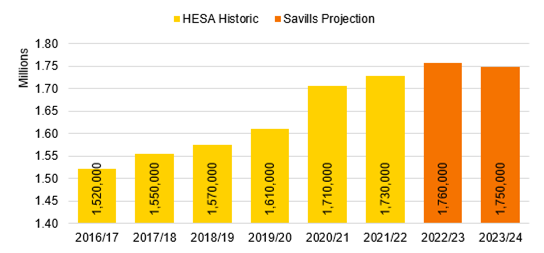

1 million applicants expected by 2030

The latest UCAS application data reveals that the number of students starting their undergraduate degree has topped 600,000 for the second year in a row – with 618,000 starting in 2022/23 and 622,000 in 2023/24. This equates to a first year cohort larger than the population of Sheffield looking for accommodation each year.

Even more growth in demand is expected, with UCAS projecting that the UK could reach 1 million university applicants in 2030, which will place existing PBSA stock under even greater pressure.

Graph 1: Total undergraduate population is forecast to surpass 1.75 million

Source: Savills using HESA, UCAS (the projections allow for a dropout rate of 6.5%pa, the average over the past 5 years)

“The UK remains one of the key global destinations for students looking to study abroad. There are currently more than 600,000 full-time international students, up from just over 400,000 five years ago, according to figures from HESA. While there has been a fall in EU students in the wake of Brexit, this has been more than offset by significant growth in the number of students from India, as well as continued strong numbers from China and elsewhere,” says James Hanmer, Head of UK PBSA Investment and Co-living, in the Operational Capital Markets division at Savills.

“We know that strong application figures from these countries are a huge positive for PBSA demand: international students are 60% more likely to live in PBSA than domestic students, with those from India more than twice as likely.”

Significant shortage of stock in some markets

Regulatory and tax changes have seen the number of buy-to-let mortgage redemptions reach over 300,000 since 2017, and as a result there are currently 31% fewer 5+ bed properties listed for rent in Q1 2023 compared with the pre-pandemic average.

This creates an even greater need for PBSA, and yet the total pipeline of new stock is only 144,000 beds nationally (on schemes with at least 20 beds), according to Savills analysis of data from Glenigan, with only a quarter of these under construction. As a result, occupancy levels are at record highs, supporting rental growth of around 7%, according to Unite and Empiric, which is expected to drive continued strong investment returns over the coming years.

Savills PBSA Development League Table indicates particularly strong development opportunities in Canterbury, Durham and Glasgow (around the University of Glasgow), all of which have seen strong growth in their student populations, with the former two also seeing rising applications, which will put pressure on existing stock. They have been promoted to First Class in the Savills league table, joining Bath, Birmingham, Brighton, Edinburgh, London, Manchester, Oxford and St Andrews, all cities with very high student demand.

Southampton, Bournemouth and Cambridge have moved up to the Upper Second tier of the Savills league table, as rising student numbers put pressure on existing stock and with a relatively limited pipeline of new schemes to meet those increases.

Investment activity remains strong despite the challenging backdrop

In spite of the weaker macro-economic backdrop, which saw overall real estate investment in the UK down by -14.2% in 2022, PBSA bucked the trend with a record-breaking £7.8 billion of stock traded – an increase of +89% on 2021 figures.

Over the past three years, 82% of investment in UK PBSA has come from overseas, with investors from USA and Singapore accounting for 47% and 24% respectively over this period.

While investment has been limited to date in 2023, activity is expected to pick up in the second half of the year, supported by rising rents, which are offsetting the challenges faced, including operational cost increases. Savills recent European Living Investor Survey found that around two-thirds of investors are looking to deploy more capital into PBSA over the next three years. Of investors looking to expand in the sector, close to a fifth expect to deploy more than €500 million by 2025.

“The current supply and demand dynamics create a compelling opportunity for investors to deliver much-needed new PBSA, in particular to target the growing domestic student population. The underlying student growth demonstrates the long-term demand for PBSA and underpins the attractiveness of investment in the sector,” comments Richard Valentine-Selsey, Head of European Living Research & Consultancy at Savills.

“While build costs increased significantly over the past two years, reaching just under 10% in 2022, putting pressure on the deliverability of some schemes, the latest forecasts suggest that the worst of the price rises are behind us. Tender price inflation is forecast to fall back to just 2-3% per annum for 2023 and 2024, which should bring some confidence and increased viability back to the development of new PBSA stock.”

Savills latest research also highlights that despite economic environment and implications of higher interest rates, early indicators from the debt market in 2023 reveal that demand from lenders to finance both development and investment opportunities in the PBSA sector remains strong, particularly for quality projects and strong sponsors.

Charlie Bottomley, Director in Savills Debt Advisory team, said, “All lenders, including banks, insurance companies and debt funds, are showing considerable appetite for the sector, as they recognise its resilience and strong rental growth performance. Interestingly, the increase in base rates has created a convergence of pricing between bank and nonbank lenders, particularly for development finance. For a marginal increase in all-in debt costs, non-bank lenders are offering a meaningful increase in leverage, which typically results in a positive impact on equity IRR”.